In the dynamic landscape of investment, the quest for maximum returns is an ever-present pursuit. As an investor, your journey is paved with a multitude of options, each carrying its own set of risks and rewards. Among these options, one avenue that deserves your attention is investing in different types of notes. Note offer a unique blend of flexibility, diversification, and potential for impressive returns. In this guide, we will embark on a journey of exploration into various note types, deciphering their intricacies, benefits, and considerations to help you make informed investment decisions.

Understanding the Note Basics: What Are Notes?

Before delving into the various note types, let’s establish a fundamental understanding of what notes are. In essence, it is a debt instrument—an agreement between an issuer (usually a borrower) and an investor (lender). The issuer borrows funds from the investor and promises to repay the principal amount along with interest over a predetermined period. Notes can take different forms, each designed to cater to different investment goals and risk tolerances.

Investors seeking maximum returns should prioritize comprehensive research and strategic planning. Begin by taking meticulous notes during market analysis, tracking trends, and studying historical data. These notes serve as valuable references, aiding in informed decision-making. Utilize tools like financial statements and market reports to enhance note-taking precision. Regularly update and review these notes to adapt to evolving market conditions. Harness the power of diversified portfolios, incorporating insights from your accumulated notes to balance risk and reward effectively. Embrace a disciplined approach, aligning your investment strategy with your financial goals. In the pursuit of maximum returns, diligent note-taking becomes an indispensable ally, guiding investors towards success.

At the heart of the financial world, note stand as versatile instruments that connect borrowers and lenders in a dance of capital exchange. Imagine it as a financial agreement, a pact between two parties—one seeking funds, the other with capital to spare. Notes offer a way to formalize this transaction, providing a structure that outlines the terms, obligations, and benefits for both sides.

In simple terms, a note is a type of debt instrument. Debt, in this context, doesn’t carry the ominous weight it might in everyday conversation. Instead, it signifies a form of borrowing—an arrangement where one party borrows money from another with the promise to pay it back over time. The beauty of note lies in their adaptability, offering a range of options to suit various financial goals and preferences.

What Are the Different types of Notes?

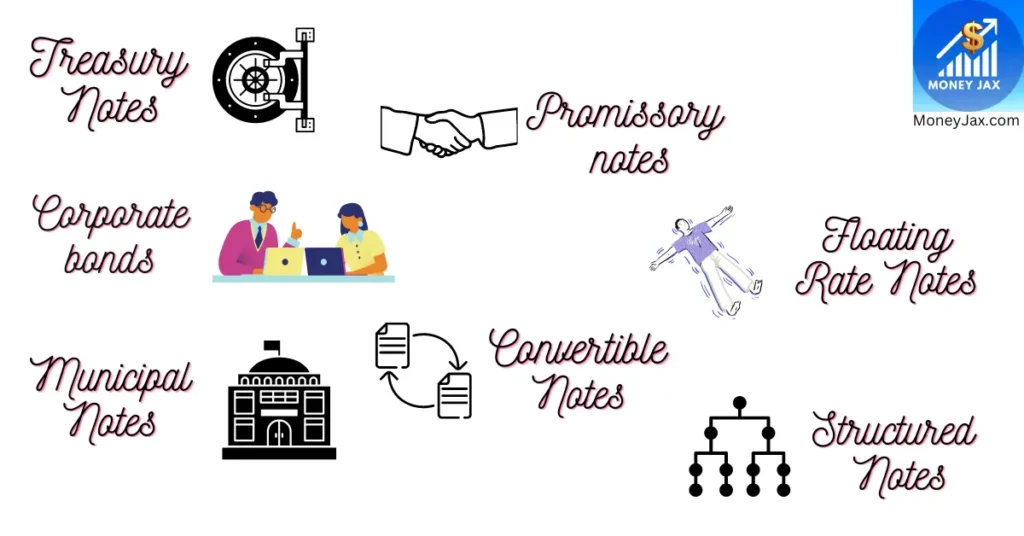

1. Treasury Notes: Stability in Uncertain Times

Treasury notes are issued by the U.S. Department of the Treasury, making them one of the most secure investment options available. These come in various maturities, typically ranging from two to ten years. One key advantage of investing in treasury note is their relative stability, backed by the full faith and credit of the U.S. government. While the returns on treasury notes might not be as high as some other investments, they offer a reliable source of income and act as a buffer during turbulent economic times.

2. Corporate Bonds: Balancing Risk and Reward

Corporate bonds are notes issued by companies to raise capital. They offer investors an opportunity to earn higher yields compared to government bonds, but with an added level of risk. The risk arises from the creditworthiness of the issuing company. Investment-grade corporate bonds are issued by financially stable companies, while high-yield (or junk) bonds are issued by companies with a higher risk of default. Investing in corporate bonds requires careful research to assess the company’s financial health and credit rating.

3. Municipal Notes: Tax-Efficient Investing

Municipal notes, also known as Munis, are issued by state and local governments to finance public projects. They offer tax advantages, as the interest earned is often exempt from federal income tax and, in some cases, state and local taxes as well. Municipal notes come in various forms, including general obligation bonds and revenue bonds. While they are generally considered safer than corporate bonds, it’s important to evaluate the financial health of the issuing municipality before investing.

4. Promissory Notes: Tailored Returns Through Private Lending

Promissory notes are unique in that they often involve private lending arrangements between individuals or businesses. They offer a direct way to invest in various projects, such as real estate or small businesses, while negotiating terms with the borrower. This avenue provides more control and potentially higher returns, but it also comes with increased risk due to the lack of regulatory oversight and the borrower’s creditworthiness.

5. Convertible Notes: Balancing Debt and Equity

Convertible notes bridge the gap between debt and equity investments. These notes are issued by startups and small companies looking to raise capital. They start as debt instruments, promising interest payments and repayment of the principal. However, they can be converted into equity (ownership) in the issuing company under certain conditions, such as during a future funding round. Convertible notes offer the potential for substantial returns if the company succeeds, but they also carry the risk of loss if the company struggles.

6. Floating Rate Notes: Navigating Interest Rate Changes

Floating rate notes, also known as floaters, come with interest rates that adjust periodically based on a reference rate, such as the U.S. Treasury bill rate. These notes are designed to provide protection against rising interest rates. As interest rates increase, the interest paid on floating rate notes also rises, helping investors maintain purchasing power. Floaters are particularly attractive in environments where interest rates are expected to rise.

7. Structured Notes: Customized Exposure

Structured notes are complex instruments that combine traditional debt securities with derivatives. These notes offer exposure to a specific market index, commodity, or other underlying assets, allowing investors to customize their exposure and potential returns. However, structured notes can be intricate and involve various risks, including potential losses if the underlying asset performs poorly.

Here’s a closer look at how notes operate:

The Players: Issuer and Investor

In the world of notes, two key characters take center stage: the issuer and the investor. The issuer is typically an entity in need of funds—this could be the U.S. government, a corporation, a municipality, a startup, or even an individual. On the other side, the investor is someone who has the financial capacity to lend money. This could be you, me, a financial institution, or any entity looking to grow its wealth through lending.

The Agreement: Promissory Nature

At its core, a note is a promise. It’s a formal agreement wherein the issuer promises to repay the borrowed funds, also known as the principal amount, to the investor after a predetermined period. This repayment doesn’t happen all at once but is spread out over time, often in installments. In return for lending their funds, investors receive interest—a sort of compensation for allowing their money to be tied up for the specified period.

Variety in Form and Purpose

Notes come in a dazzling array of forms, each tailored to specific needs and circumstances. Some notes are issued by governments to fund public projects or manage financial activities, while others are crafted by companies to finance their operations or expansion plans. There are also note that cater to personal financing arrangements, facilitating private lending between individuals or businesses.

Security and Returns: The Yin and Yang

When considering notes, security and returns take center stage in the decision-making process. On one hand, there’s the allure of higher returns, the possibility of your money growing substantially over time. On the other hand, there’s the need for security—to ensure that your investment doesn’t evaporate due to unforeseen circumstances. This interplay between security and returns is a defining feature of notes, and investors often find themselves striking a balance between the two.

The Big Picture: A Complex Financial Ecosystem

Zooming out, they are an integral part of the financial ecosystem. They facilitate the flow of funds, enabling governments, companies, and individuals to access the capital they need to operate, innovate, and grow. They also provide opportunities for investors to multiply their wealth, diversify their portfolios, and participate in various sectors of the economy.

In essence, notes embody the essence of capitalism—an intricate web of financial relationships built on trust and the promise of mutual benefit. As you delve into the world of investing and explore the various types that are available, remember that they are more than just pieces of paper or digital entries on a screen. They are the bridges that connect the dreams and ambitions of issuers with the resources and aspirations of investors, shaping the financial landscape in the process.

Maximizing Returns and Managing Risk

When it comes to investing in different note types for maximum returns, a well-balanced approach is essential. Diversification, which involves spreading your investments across various asset classes, sectors, and note types, is a key strategy for managing risk while aiming for attractive returns.

Consider your investment goals, risk tolerance, and time horizon when selecting note types to include in your portfolio. Conservative investors might lean more toward Treasury notes and investment-grade corporate notes, while those seeking higher yields could explore municipal notes or higher-risk corporate notes.

It’s also important to conduct thorough research on the issuers before investing in any note type. Assess the issuer’s financial health, creditworthiness, and market conditions that could impact the note’s performance.

Making Informed Decisions: Factors to Consider

While exploring these diverse note types, it’s crucial to consider several factors before making investment decisions:

1. Risk Tolerance: Different note types come with varying degrees of risk. Assess your risk tolerance and investment goals before allocating funds to specific note types.

2. Time Horizon: Consider the length of time you can commit to an investment. Some notes have shorter maturities, while others require a longer investment horizon.

3. Market Conditions: Economic conditions, interest rate trends, and market volatility can impact note values. Stay informed about macroeconomic trends that could affect your investments.

4. Due Diligence: Thoroughly research the issuing entity’s financial health, credit rating, and track record. This step is crucial, especially for corporate bonds, municipal notes, and private lending arrangements.

5. Diversification: Spread your investments across different note types to reduce the impact of poor performance in any one area.

6. Tax Implications: Consider the tax implications of your investments. Municipal notes, for example, offer tax benefits, while interest from other note types may be subject to taxation.

7. Investment Goals: Align your note investments with your overall investment strategy and goals. Are you seeking stable income, capital appreciation, or a combination of both?

Conclusion: Empowered Investment Choices

As you embark on your journey of exploring different note types for maximum returns, the factors outlined above form a comprehensive framework for making informed investment decisions. Remember that investment decisions should be driven by a clear understanding of your personal circumstances, financial goals, and risk tolerance.

The intricate interplay between risk and reward necessitates thoughtful consideration at every step. By assessing your risk tolerance, understanding your time horizon, staying informed about market conditions, conducting due diligence, diversifying wisely, accounting for tax implications, and aligning with your investment goals, you can create a portfolio of note investments that align with your aspirations and provide a solid foundation for your financial future.

Ultimately, the path to maximum returns is uniquely yours to navigate. Armed with knowledge, foresight, and a willingness to adapt, you can confidently traverse the investment landscape, optimizing returns while effectively managing risk. Your journey as a savvy investor is an ongoing exploration—one that holds the promise of potential rewards as you make empowered choices that steer you toward your financial ambitions.

Remember, the investment landscape is constantly evolving, and staying informed about market trends, economic shifts, and regulatory changes will position you as a savvy investor ready to capitalize on opportunities while managing risks effectively. So, embark on this journey armed with knowledge, and may your exploration into the world of notes yield fruitful returns for your financial future.

Also Read:

Frequently Asked Questions

What are notes in investment?

Notes are debt instruments where an investor lends money to an issuer (like a government or company) in exchange for repayment with interest over a set period.

What is the advantage of investing in Treasury Notes?

Treasury Notes, backed by the U.S. government, provide stability and lower risk due to their reliable repayment record.

How do Convertible Notes work?

Convertible Notes start as loans but can be converted into ownership (equity) in a company during future funding rounds, offering potential for high returns.

What is the purpose of Floating Rate Notes?

Floating Rate Notes adjust interest rates based on market changes, making them a smart choice to counter rising interest rates and preserve purchasing power.

What should investors consider before investing in notes?

Investors should assess risk tolerance, investment goals, market conditions, due diligence, diversification, tax implications, and alignment with overall strategy.

1 thought on “Exploring Different Types of Notes for Maximum Returns: A Guide for Savvy Investors in 2026”