Purchasing a home is a significant milestone for many Americans, and for most, it involves securing a mortgage loans. A mortgage loan is a financial tool that empowers individuals and families to realize their homeownership dreams by providing the necessary funds to purchase a property. In this comprehensive guide, we will break down the intricacies of mortgage loans, offering a clear and accessible overview for U.S. audiences. From understanding the basics to making informed decisions, we will explore every aspect of mortgage loans in human and easy language.

What is a Mortgage Loans?

A mortgage loan is a financial arrangement that enables individuals to purchase real estate, usually a home, without having to pay the full purchase price upfront. It’s a type of secured loan, where the property being purchased serves as collateral(security) for the loan. The primary purpose of a mortgage loans is to provide individuals with the means to achieve homeownership by spreading the cost of the property over an extended period. This allows borrowers to make manageable monthly payments over the life of the loan, rather than paying the entire purchase price at once.

In summary, a mortgage loan is a financial tool that empowers individuals to become homeowners by borrowing money to purchase property. It involves various terms, interest rates, and payment structures, all of which are tailored to help borrowers achieve their homeownership goals while managing their financial obligations responsibly.

Mortgage loans play a pivotal role in facilitating home ownership. These financial instruments empower individuals to purchase real estate by providing substantial capital upfront. Lenders, typically banks or financial institutions, extend mortgage loans with agreed-upon interest rates and repayment terms. Prospective homeowners must undergo a comprehensive application process, which includes credit checks and income verification. The borrowed funds are secured by the property itself, minimizing risks for lenders. Repayment occurs over an extended period, often spanning decades, making homeownership accessible to a broader demographic. Mortgage loans are integral to the real estate market, fostering economic growth by supporting property transactions and enabling families to establish roots in their own homes.

Types of Mortgage Loans

In the realm of mortgage loans, various options cater to the diverse needs of homebuyers. Let’s explore the different types of mortgage loans and their unique characteristics:

- Fixed-Rate Mortgage: A fixed-rate mortgage offers stability and predictability. In this type of loan, the interest rate remains constant throughout the loan term. This means that your monthly payments will stay the same, making it easier to budget and plan for the future. Fixed-rate mortgages are a popular choice for individuals who prefer consistent payments and want to lock in a favorable interest rate.

- Adjustable-Rate Mortgage (ARM): An adjustable-rate mortgage, or ARM, presents a dynamic option. The interest rate starts off lower than that of a fixed-rate mortgage for a specified initial period, which could be anywhere from a few months to several years. After this period, the interest rate adjusts periodically based on a specific index. While ARMs offer lower initial payments, they come with the potential for fluctuating payments in the future.

- FHA Loans (Federal Housing Administration): FHA loans are government-backed loans designed to help first-time homebuyers and individuals with lower credit scores. They make homeownership more accessible by setting a lower down payment. FHA loans also offer competitive interest rates and have more flexible qualification requirements. However, they do require mortgage insurance premiums to protect the lender in case of default.

- VA Loans (Department of Veterans Affairs): VA loans are exclusively available to eligible veterans, active-duty service members, and certain members of the National Guard and Reserves. These loans require no down payment and offer favorable terms, such as competitive interest rates and limited closing costs. VA loans aim to honor the service of military personnel by providing them with an opportunity to achieve homeownership.

- USDA Loans (United States Department of Agriculture): USDA loans are intended to promote homeownership in rural and suburban areas. These loans require no down payment and offer low-interest rates. Eligibility for USDA loans is determined by income and property location. They are an excellent option for those seeking affordable homeownership in less densely populated areas.

- Jumbo Loans: Jumbo loans are tailored for homebuyers seeking to purchase high-value properties that exceed the conforming loan limits set by government-sponsored enterprises (GSEs). Since these loans exceed the limits, they often come with stricter credit requirements and higher down payments. Jumbo loans provide the necessary financing for luxury homes and upscale properties.

Each of these mortgage loan types serves a distinct purpose and comes with its own set of benefits and considerations. Understanding these options empowers homebuyers to make informed decisions that align with their financial goals and circumstances. Whether you prioritize stability, flexibility, or specialized assistance, there’s a mortgage loan type suited to your unique homeownership journey.

Key Components of a Mortgage Loan

When it comes to understanding the inner workings of a mortgage loan, several key components play a pivotal role in shaping the terms and conditions of your home financing. Let’s delve into these fundamental elements that collectively define your mortgage journey.

- Principal and Interest: The cornerstone of any mortgage loan is the concept of principal and interest. The principal refers to the initial amount borrowed to purchase your home, while interest represents the additional cost you pay to the lender for borrowing that money. As you make your monthly mortgage payments, a portion goes toward reducing the principal, thereby increasing your equity in the property, and another portion covers the interest accrued on the outstanding balance. Over time, the balance between principal and interest payments shifts, with more of your payment going toward reducing the principal.

- Down Payment: The down payment is a crucial upfront payment made by the homebuyer at the time of purchase. It is usually expressed as a percentage of the total purchase price of home. A higher down payment often results in a lower loan amount, which can lead to more favorable interest rates and reduced monthly payments. The down payment demonstrates your commitment to the purchase and also serves as a buffer for the lender in case the value of the property declines.

- Loan Term: The loan term refers to the duration over which you will repay the mortgage loan. Common loan terms include 15, 20, or 30 years, although other options may be available. Shorter loan terms typically come with higher monthly payments but lower overall interest costs, while longer terms offer lower monthly payments but result in higher overall interest expenses. Selecting the right loan term depends on your financial goals, budget, and future plans.

- Interest Rate Types: Mortgage loans offer various interest rate options, each with its own implications for your monthly payments and the overall cost of the loan. The two primary interest rate types are fixed-rate and adjustable-rate mortgages (ARMs). A fixed-rate mortgage maintains a constant interest rate throughout the loan term, providing predictability and stability in payments. On the other hand, an ARM features an interest rate that may change periodically, typically after an initial fixed period. This can lead to fluctuating payments, with potential for both increases and decreases in the interest rate over time. Choosing between these options requires careful consideration of your risk tolerance and financial circumstances.

Understanding these key components is essential for making informed decisions when navigating the mortgage loan landscape. Your choice of principal and interest structure, down payment amount, loan term, and interest rate type will collectively shape your homeownership experience, impacting your finances and long-term goals. As you embark on your journey to homeownership, take the time to familiarize yourself with these components and their implications, enabling you to confidently select the mortgage loan that aligns with your aspirations.

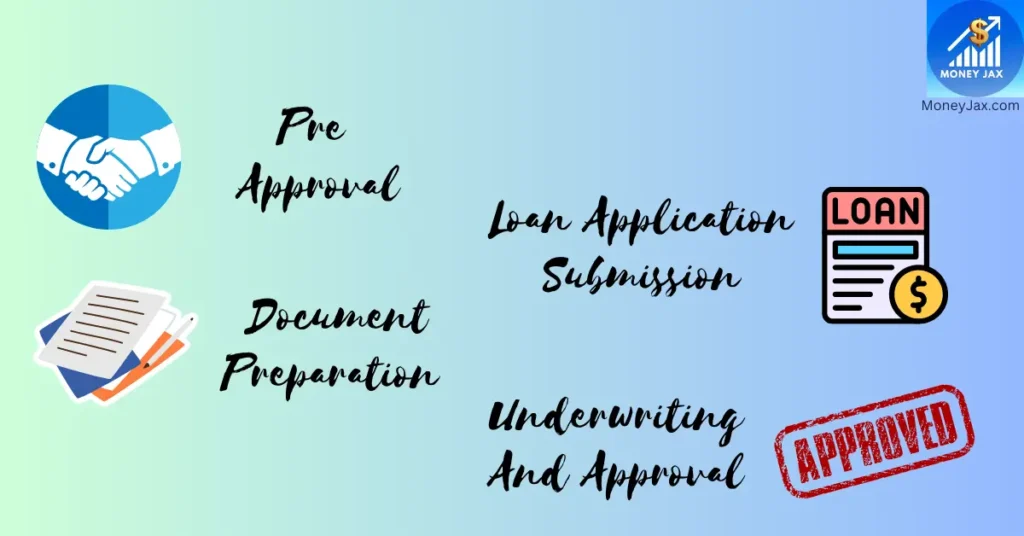

The Mortgage Application Process

The process of applying for a mortgage loan involves several crucial steps that culminate in securing the necessary funds for purchasing a home. Let’s delve into the key terms within the mortgage application process:

Pre-Approval:

Pre-approval is an essential initial step in the mortgage application process. It involves prospective homebuyers providing their financial information to a lender, who then evaluates their credit history, income, and other relevant factors to determine the maximum loan amount they qualify for. Pre-approval helps individuals set a realistic budget for house hunting, streamlining the search by narrowing down options that fit within their financial means.

Document Preparation:

Once pre-approved, the next step is document preparation. This stage requires gathering and organizing various financial documents that the lender will need to assess the borrower’s financial stability and creditworthiness. These documents may include tax returns, pay stubs, bank statements, and employment verification. Ensuring accurate and comprehensive document submission is vital to facilitate a smooth loan application process.

Loan Application Submission:

With the necessary documents in hand, the borrower submits a formal loan application to the lender. This application includes details about the property being purchased, the requested loan amount, the borrower’s financial information, and other pertinent details. Submitting the application triggers the lender’s official review and evaluation of the borrower’s eligibility for the mortgage loan.

Underwriting and Approval:

The underwriting process is where the lender meticulously assesses the borrower’s financial information, credit history, and the property itself to determine whether to approve the mortgage loan. Underwriters analyze the borrower’s ability to repay the loan, the property’s value, and its potential as collateral. If the underwriter approves the application, the borrower receives a formal loan approval, which signifies that they meet the lender’s criteria and are cleared to proceed with the purchase. This approval is a critical milestone that brings borrowers one step closer to realizing their homeownership dreams.

In essence, the mortgage application process involves progressing through these stages – from pre-approval to underwriting and approval – ensuring that all necessary documentation is provided and reviewed to secure the mortgage loan needed to purchase a new home. Each step is integral to the overall process, and a successful journey through these stages sets the foundation for a successful and fulfilling homeownership experience.

Understanding Interest Rates

Interest rates play a pivotal role in your mortgage journey. These rates are influenced by various factors, including economic indicators such as inflation, employment rates, and the overall health of the economy. Lenders also consider the term of your loan and the type of loan you choose. Mortgage points are another factor affecting interest rates. These are fees paid upfront to lower your interest rate, effectively reducing your monthly payments. Additionally, “locking in” your interest rate is a strategy that allows you to secure a favorable rate for a specific period, shielding you from potential rate fluctuations.

The Role of Credit Scores

Credit scores wield significant influence over your mortgage application. Lenders use these scores to assess your creditworthiness and determine the interest rate you qualify for. A higher credit score often results in a lower interest rate, potentially saving you thousands of dollars over the life of your loan. If your credit score needs improvement, take proactive steps to enhance it. Paying bills on time, reducing debt, and managing your credit responsibly can all contribute to a healthier credit score, positively impacting your mortgage terms.

Down Payments and Private Mortgage Insurance (PMI)

The down payment you make on your home has a direct bearing on your mortgage terms. While there is no fixed “optimal” down payment, a larger down payment can lead to lower monthly payments and reduced interest costs. On the other hand, if your down payment is less than 20% of the home’s value, lenders often require you to have Private Mortgage Insurance (PMI). PMI safeguards the lender in case of default but adds an extra cost to your monthly payments. Understanding PMI and its implications is essential to making an informed decision about your down payment and long-term homeownership costs.

Avoiding Common Mortgage Mistakes

- Overextending Yourself: One of the most critical aspects of securing a mortgage loan is to avoid overextending yourself financially. This means not committing to a mortgage payment that stretches your budget to the breaking point. Overextending can lead to financial stress and potentially put your homeownership at risk if you struggle to make your mortgage payments.

- Ignoring Pre-Approval: Prior to beginning your home search, it’s essential to seek pre-approval from a lender. Ignoring this crucial step can lead to disappointment and wasted time. Pre-approval gives you a clear understanding of your budget and shows sellers that you’re a serious buyer, potentially giving you an edge in a competitive housing market.

- Not Shopping Around: Failing to shop around for mortgage options can be a costly mistake. Different lenders offer various terms, interest rates, and fees. Not exploring multiple options might result in missing out on more favorable terms that could save you thousands of dollars over the life of your loan.

Choosing the Right Lender

- Banks vs. Credit Unions vs. Online Lenders: When it comes to choosing a lender for your mortgage, you have several options, including traditional banks, credit unions, and online lenders. Each has its advantages and disadvantages. Banks offer familiarity and in-person service, while credit unions often provide competitive rates and a community focus. Online lenders offer convenience and potentially faster processes. Choosing the right lender involves assessing your preferences, needs, and the terms they offer.

- Working with Mortgage Brokers: Mortgage brokers act as intermediaries between borrowers and multiple lenders. They can help you find the most suitable mortgage based on your financial situation and goals. Brokers have access to a variety of lending options and can potentially secure better terms for you. However, it’s crucial to research and choose a reputable and experienced broker who has your best interests in mind.

Navigating the mortgage process involves making informed decisions and avoiding common pitfalls. By being mindful of these aspects, such as avoiding overextending yourself and shopping around for lenders, as well as choosing the right type of lender, you can increase your chances of securing a mortgage that aligns with your financial situation and homeownership goals.

Learn more about Mortgage Loan:

Conclusion

Purchasing a home is a journey that requires careful planning and understanding. Mortgage loans are powerful tools that enable individuals and families to step into homeownership, but they come with a set of responsibilities and complexities. This comprehensive guide has aimed to demystify the world of mortgage loans, breaking down every crucial aspect in an accessible and human manner. From the basics of mortgage types to the intricacies of interest rates and credit scores, armed with this knowledge, you can confidently navigate the process of securing a mortgage loan. Remember, informed decisions today pave the way for a brighter homeownership future tomorrow.

Also read:

Frequently Asked Questions

What is a mortgage loan?

A mortgage loan is a type of financial arrangement where a lender provides funds to a borrower to purchase a home, with the property itself serving as collateral. The borrower repays the loan over a specified period, typically through monthly installments.

How do I qualify for a mortgage loan?

To qualify for a mortgage loan in the U.S., lenders assess factors like credit score, income, employment history, and debt-to-income ratio. A higher credit score, stable income, and lower debt relative to income increase your chances of approval.

What are the different types of mortgage loans?

Common types include fixed-rate (interest remains constant), adjustable-rate (interest changes over time), FHA (government-insured), and VA (veterans/military). Each has unique terms and eligibility criteria.

How much down payment is required?

Down payment requirements vary but often range from 3% to 20% of the home’s purchase price. Some loan programs, like VA or USDA loans, offer lower or no down payment options.

What’s the mortgage application process like?

After selecting a lender, you’ll submit an application with personal, financial, and property information. The lender evaluates your application, conducts a home appraisal, and decides on loan approval. If approved, you’ll finalize the loan terms and close on the property.